1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

| import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

#指定图像样式

plt.style.use('seaborn-v0_8')

#指定字体,防止中文出现乱码,windows系统指定为‘SimHei’

plt.rcParams['font.sans-serif'] = ['SimHei']

#这行代码让中文的负号“-”可以正常显示

plt.rcParams["axes.unicode_minus"]=False

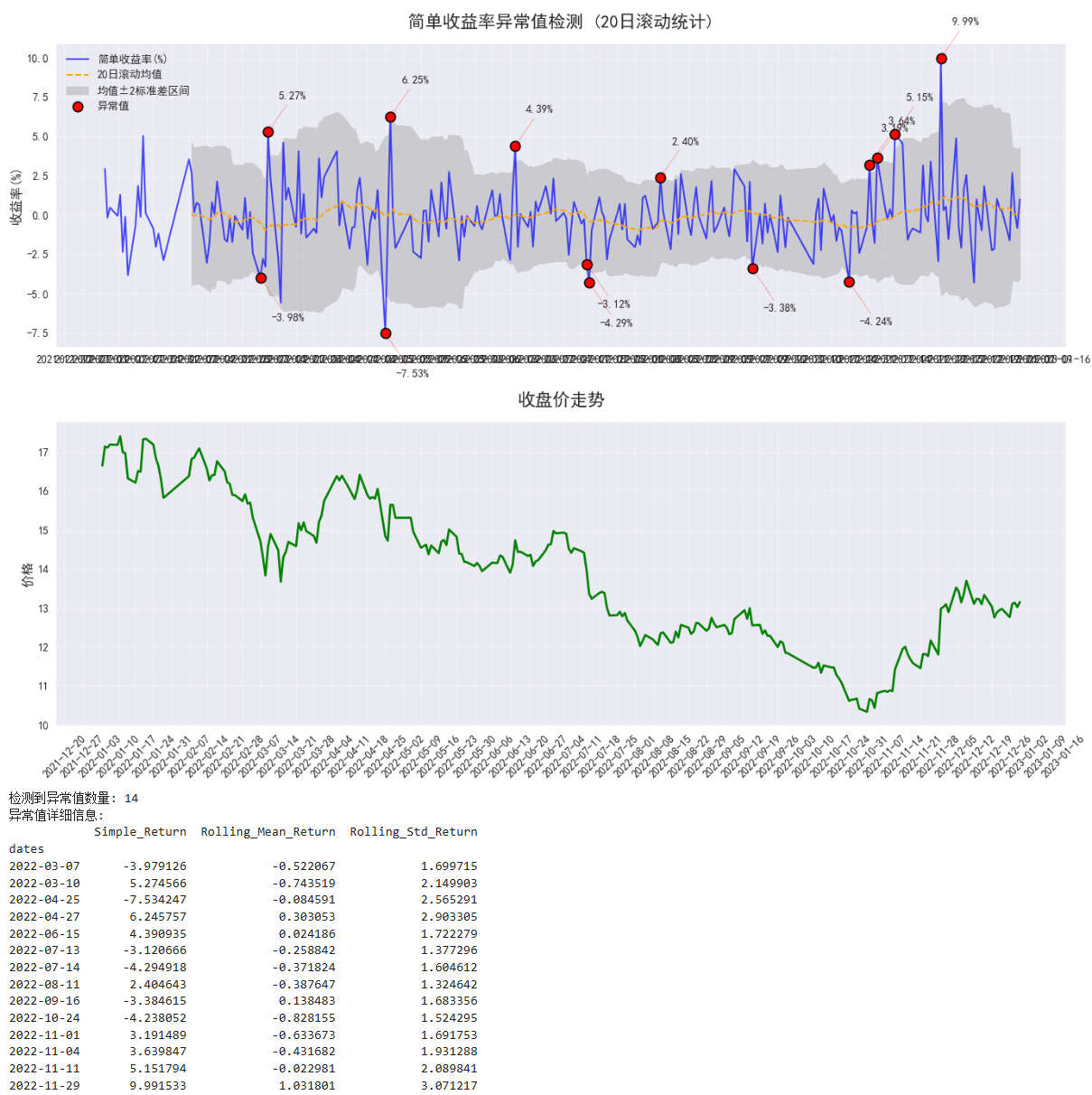

# 1. 创建示例数据(替换为你的实际数据)

df = pd.read_excel('../数据/2-1.xlsx')

df = df[['日期', '收盘']]

df.columns = ['dates','Close']

df['dates'] = pd.to_datetime(df['dates'])

df.set_index('dates', inplace = True)

# 2. 计算简单收益率(日收益率)

df['Simple_Return'] = df['Close'].pct_change() * 100 # 转换为百分比形式[8](@ref)

# 3. 计算20日滚动统计量

window_size = 20

df['Rolling_Mean_Return'] = df['Simple_Return'].rolling(window=window_size).mean()

df['Rolling_Std_Return'] = df['Simple_Return'].rolling(window=window_size).std()

# 4. 计算上下边界和异常值

df['Upper_Bound'] = df['Rolling_Mean_Return'] + 2 * df['Rolling_Std_Return']

df['Lower_Bound'] = df['Rolling_Mean_Return'] - 2 * df['Rolling_Std_Return']

df['Is_Outlier'] = (df['Simple_Return'] > df['Upper_Bound']) | (df['Simple_Return'] < df['Lower_Bound'])

# 5. 可视化

plt.figure(figsize=(14, 10), dpi=100)

# 创建子图布局

ax1 = plt.subplot(2, 1, 1) # 收益率和异常值

ax2 = plt.subplot(2, 1, 2, sharex=ax1) # 收盘价

# 绘制简单收益率和滚动统计

ax1.plot(df.index, df['Simple_Return'], label='简单收益率(%)', color='blue', alpha=0.7, linewidth=1.5)

ax1.plot(df.index, df['Rolling_Mean_Return'], label='20日滚动均值', color='orange', linestyle='--', linewidth=1.5)

ax1.fill_between(df.index, df['Upper_Bound'], df['Lower_Bound'],

color='gray', alpha=0.3, label='均值±2标准差区间')

# 标记异常值

outliers = df[df['Is_Outlier']]

ax1.scatter(outliers.index, outliers['Simple_Return'],

color='red', s=80, zorder=5,

label='异常值', edgecolors='black', linewidth=1.2)

# 添加标注文本

for date, return_val in zip(outliers.index, outliers['Simple_Return']):

ax1.annotate(f'{return_val:.2f}%',

xy=(date, return_val),

xytext=(10, 30 if return_val > 0 else -40),

textcoords='offset points',

arrowprops=dict(arrowstyle="->", color='red', alpha=0.7))

# 绘制收盘价

ax2.plot(df.index, df['Close'], label='收盘价', color='green', linewidth=2)

# 设置图表格式

ax1.set_title('简单收益率异常值检测 (20日滚动统计)', fontsize=16, pad=15)

ax1.set_ylabel('收益率(%)', fontsize=12)

ax1.legend(loc='upper left', framealpha=0.9)

ax1.grid(alpha=0.3)

ax2.set_title('收盘价走势', fontsize=16, pad=15)

ax2.set_ylabel('价格', fontsize=12)

ax2.grid(alpha=0.3)

# 设置日期格式

ax1.xaxis.set_major_formatter(mdates.DateFormatter('%Y-%m-%d'))

ax1.xaxis.set_major_locator(mdates.WeekdayLocator(byweekday=mdates.MO))

plt.xticks(rotation=45)

plt.tight_layout()

# 显示图表

plt.show()

# 6. 输出异常值统计信息

print(f"检测到异常值数量: {len(outliers)}")

print("异常值详细信息:")

print(outliers[['Simple_Return', 'Rolling_Mean_Return', 'Rolling_Std_Return']])

|