1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

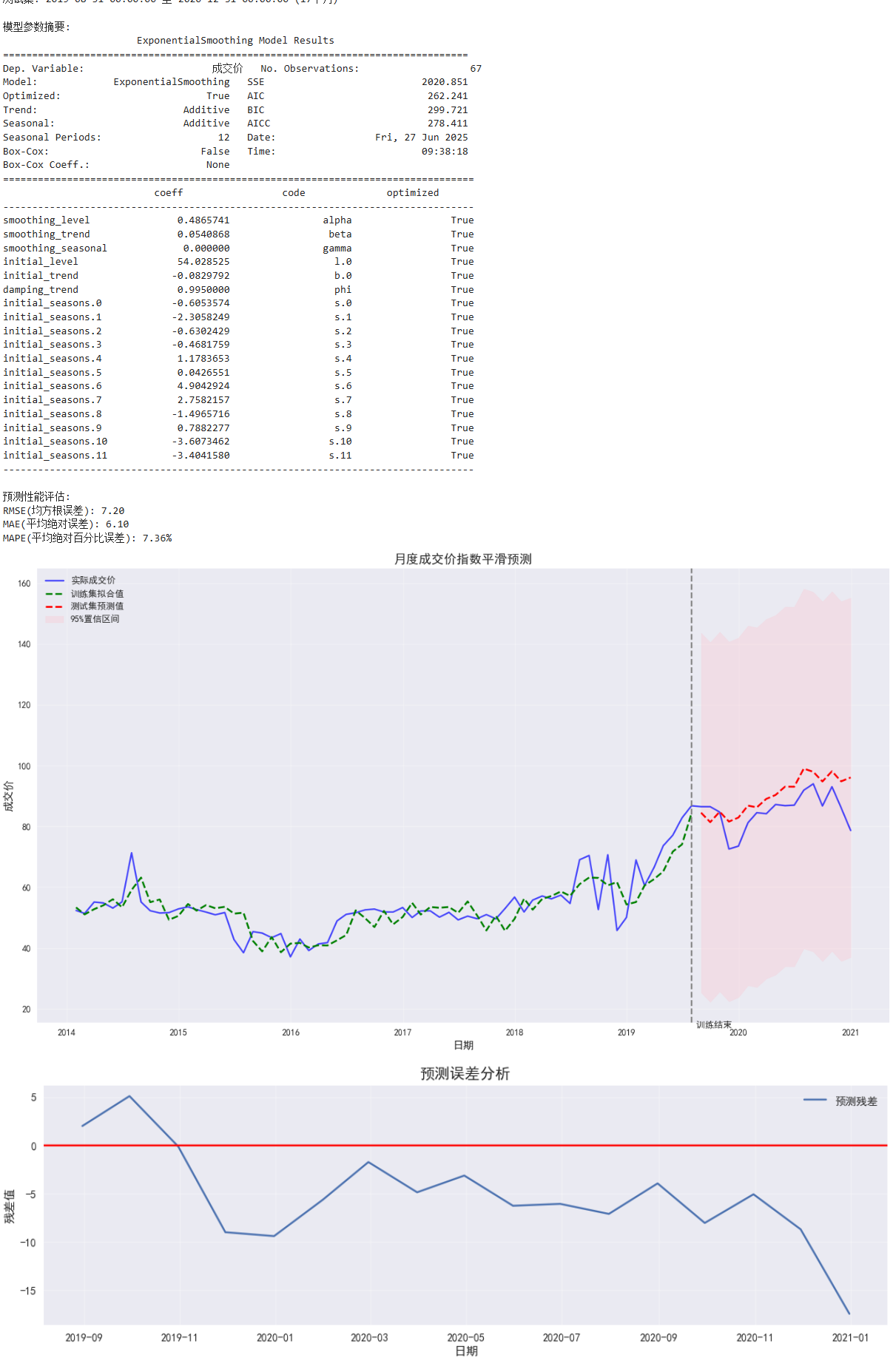

| import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from statsmodels.tsa.holtwinters import ExponentialSmoothing

from sklearn.metrics import mean_squared_error, mean_absolute_error

from sklearn.model_selection import TimeSeriesSplit

# 1. 准备示例数据(替换为实际数据)

# dates = pd.date_range(start='2018-01-01', end='2025-06-01', freq='M')

# prices = np.cumsum(np.random.normal(0.5, 2, len(dates))) + 100 # 模拟成交价

# df = pd.DataFrame({'成交价': prices}, index=dates)

# print("原始数据示例:")

# print(df.head())

# 2. 数据拆分 - 按时间顺序划分训练集和测试集[8](@ref)

train_size = int(len(monthly_df) * 0.8) # 80%作为训练集

train = monthly_df.iloc[:train_size]

test = monthly_df.iloc[train_size:]

print(f"\n训练集: {train.index.min()} 至 {train.index.max()} ({len(train)}个月)")

print(f"测试集: {test.index.min()} 至 {test.index.max()} ({len(test)}个月)")

# 3. 模型拟合 - 使用Holt-Winters季节性指数平滑[2,6](@ref)

model = ExponentialSmoothing(

train['成交价'],

trend='add', # 加法趋势

seasonal='add', # 加法季节性

seasonal_periods=12, # 月度数据的年度季节性周期

damped_trend=True # 使用阻尼趋势防止预测发散[1](@ref)

).fit()

print("\n模型参数摘要:")

print(model.summary())

# 4. 预测测试集

forecast = model.forecast(steps=len(test))

forecast_df = pd.DataFrame(forecast, index=test.index, columns=['预测值'])

# 5. 评估预测性能

rmse = np.sqrt(mean_squared_error(test['成交价'], forecast))

mae = mean_absolute_error(test['成交价'], forecast)

mape = np.mean(np.abs((test['成交价'] - forecast) / test['成交价'])) * 100

print("\n预测性能评估:")

print(f"RMSE(均方根误差): {rmse:.2f}")

print(f"MAE(平均绝对误差): {mae:.2f}")

print(f"MAPE(平均绝对百分比误差): {mape:.2f}%")

# 6. 可视化结果

plt.figure(figsize=(14, 8))

# 绘制原始数据和拟合值

plt.plot(monthly_df.index, monthly_df['成交价'], 'b-', label='实际成交价', alpha=0.7)

plt.plot(train.index, model.fittedvalues, 'g--', label='训练集拟合值', linewidth=2)

# 绘制预测值和置信区间

plt.plot(forecast_df.index, forecast_df['预测值'], 'r--', label='测试集预测值', linewidth=2)

plt.fill_between(

forecast_df.index,

model.forecast(steps=len(test)) - 1.96 * model.sse / len(train),

model.forecast(steps=len(test)) + 1.96 * model.sse / len(train),

color='pink', alpha=0.3, label='95%置信区间'

)

# 添加分隔线和标注

plt.axvline(x=train.index[-1], color='gray', linestyle='--')

plt.text(train.index[-1], plt.ylim()[0]*0.9, ' 训练结束', fontsize=10)

# 图表装饰

plt.title('月度成交价指数平滑预测', fontsize=14)

plt.xlabel('日期', fontsize=12)

plt.ylabel('成交价', fontsize=12)

plt.grid(alpha=0.3)

plt.legend(loc='upper left')

plt.tight_layout()

# 7. 残差诊断(可选)

residuals = test['成交价'] - forecast

plt.figure(figsize=(14, 4))

plt.plot(residuals, label='预测残差')

plt.axhline(y=0, color='r', linestyle='-')

plt.title('预测误差分析', fontsize=14)

plt.xlabel('日期')

plt.ylabel('残差值')

plt.grid(alpha=0.3)

plt.legend()

plt.show()

|