1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

| import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from statsmodels.tsa.stattools import adfuller

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.tsa.arima.model import ARIMA

from sklearn.metrics import mean_squared_error

import warnings

# 忽略警告信息

warnings.filterwarnings('ignore')

# 1. 数据准备(假设df是包含日期索引和'成交价'列的DataFrame)

# 确保索引是DatetimeIndex格式

# df.index = pd.to_datetime(df.index)

# 2. 平稳性检验与差分处理

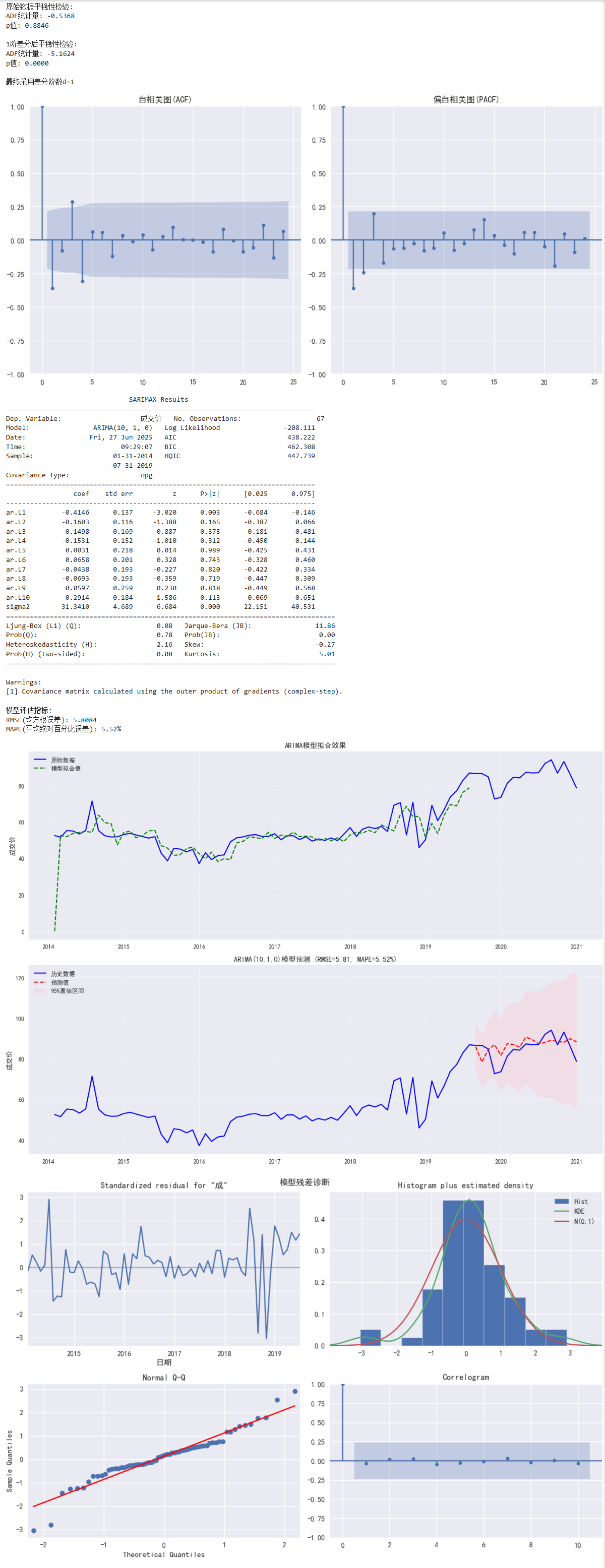

def check_stationarity(series):

"""执行ADF检验并返回结果"""

result = adfuller(series.dropna())

print(f'ADF统计量: {result[0]:.4f}')

print(f'p值: {result[1]:.4f}')

return result[1] < 0.05 # p<0.05表示平稳

# 检查原始数据平稳性

print("原始数据平稳性检验:")

is_stationary = check_stationarity(monthly_df['成交价'])

# 自动差分直到平稳

d = 0

diff_series = monthly_df['成交价'].copy()

while not is_stationary and d < 3: # 最多差分3次

d += 1

diff_series = diff_series.diff().dropna()

print(f"\n{d}阶差分后平稳性检验:")

is_stationary = check_stationarity(diff_series)

print(f"\n最终采用差分阶数d={d}")

# 3. 确定ARIMA参数(p,d,q)

# 绘制ACF和PACF图

plt.figure(figsize=(12, 6))

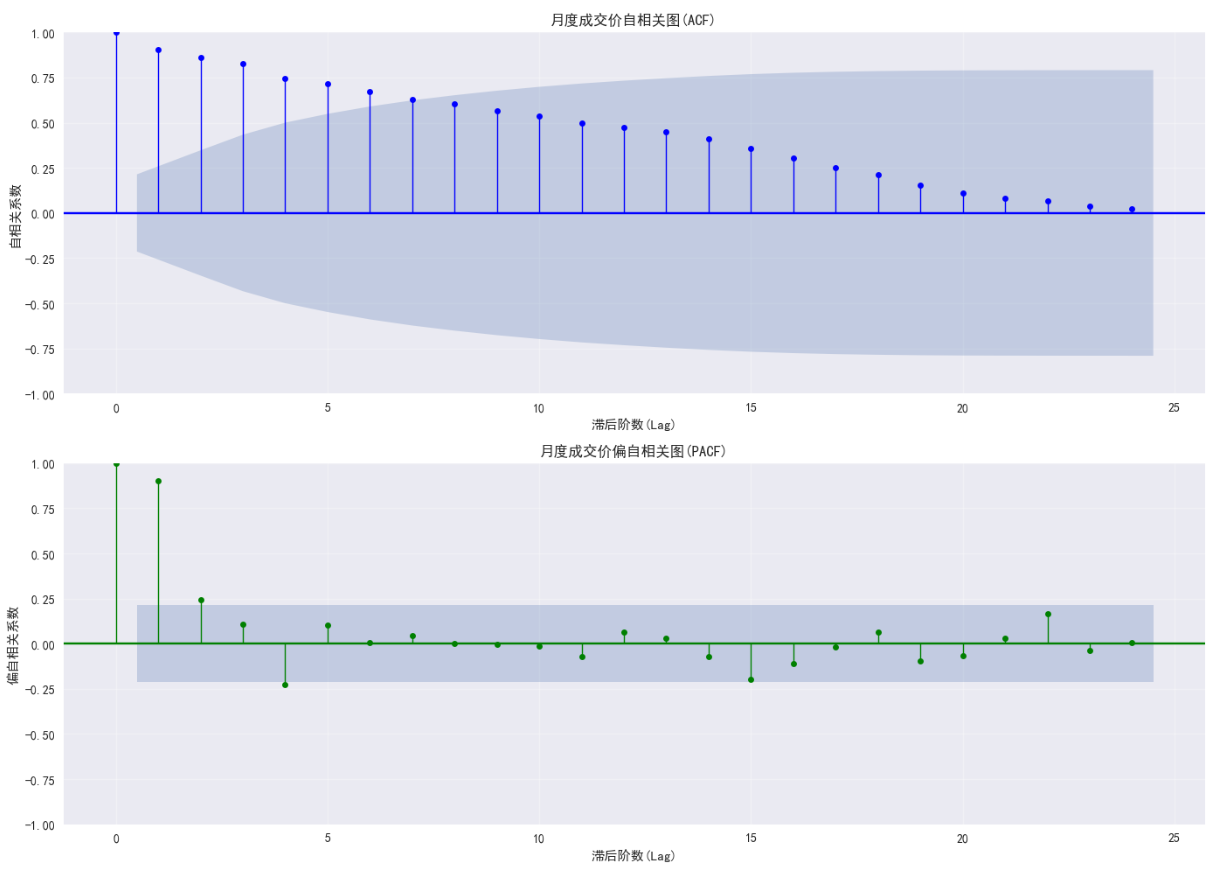

plt.subplot(121)

plot_acf(diff_series, lags=24, ax=plt.gca(), title='自相关图(ACF)')

plt.subplot(122)

plot_pacf(diff_series, lags=24, ax=plt.gca(), title='偏自相关图(PACF)')

plt.tight_layout()

plt.show()

# 4. 划分训练集和测试集

train_size = int(len(monthly_df) * 0.8) # 80%作为训练集

train = monthly_df.iloc[:train_size]

test = monthly_df.iloc[train_size:]

# 5. 拟合ARIMA模型 (参数需根据ACF/PACF调整)

p, q = 10, 0 # 根据ACF/PACF截尾情况确定 按示例10,1

model = ARIMA(train['成交价'], order=(p, d, q))

model_fit = model.fit()

print(model_fit.summary())

# 6. 模型评估

# 在测试集上进行预测

forecast = model_fit.get_forecast(steps=len(test))

forecast_mean = forecast.predicted_mean

conf_int = forecast.conf_int()

# 计算评估指标

rmse = np.sqrt(mean_squared_error(test['成交价'], forecast_mean))

mape = np.mean(np.abs((test['成交价'] - forecast_mean) / test['成交价'])) * 100

print(f'\n模型评估指标:')

print(f'RMSE(均方根误差): {rmse:.4f}')

print(f'MAPE(平均绝对百分比误差): {mape:.2f}%')

# 7. 可视化结果

plt.figure(figsize=(14, 10))

# 原始数据与拟合值

plt.subplot(2, 1, 1)

plt.plot(monthly_df.index, monthly_df['成交价'], 'b-', label='原始数据')

plt.plot(train.index, model_fit.fittedvalues, 'g--', label='模型拟合值')

plt.title('ARIMA模型拟合效果')

plt.ylabel('成交价')

plt.legend()

plt.grid(alpha=0.3)

# 预测结果与置信区间

plt.subplot(2, 1, 2)

plt.plot(monthly_df.index, monthly_df['成交价'], 'b-', label='历史数据')

plt.plot(forecast_mean.index, forecast_mean, 'r--', label='预测值')

plt.fill_between(conf_int.index,

conf_int.iloc[:, 0],

conf_int.iloc[:, 1],

color='pink', alpha=0.3, label='95%置信区间')

plt.title(f'ARIMA({p},{d},{q})模型预测 (RMSE={rmse:.2f}, MAPE={mape:.2f}%)')

plt.ylabel('成交价')

plt.legend()

plt.grid(alpha=0.3)

plt.tight_layout()

plt.show()

# 8. 残差诊断(可选)

model_fit.plot_diagnostics(figsize=(12, 8))

plt.suptitle('模型残差诊断', y=0.95)

plt.tight_layout()

plt.show()

|