1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

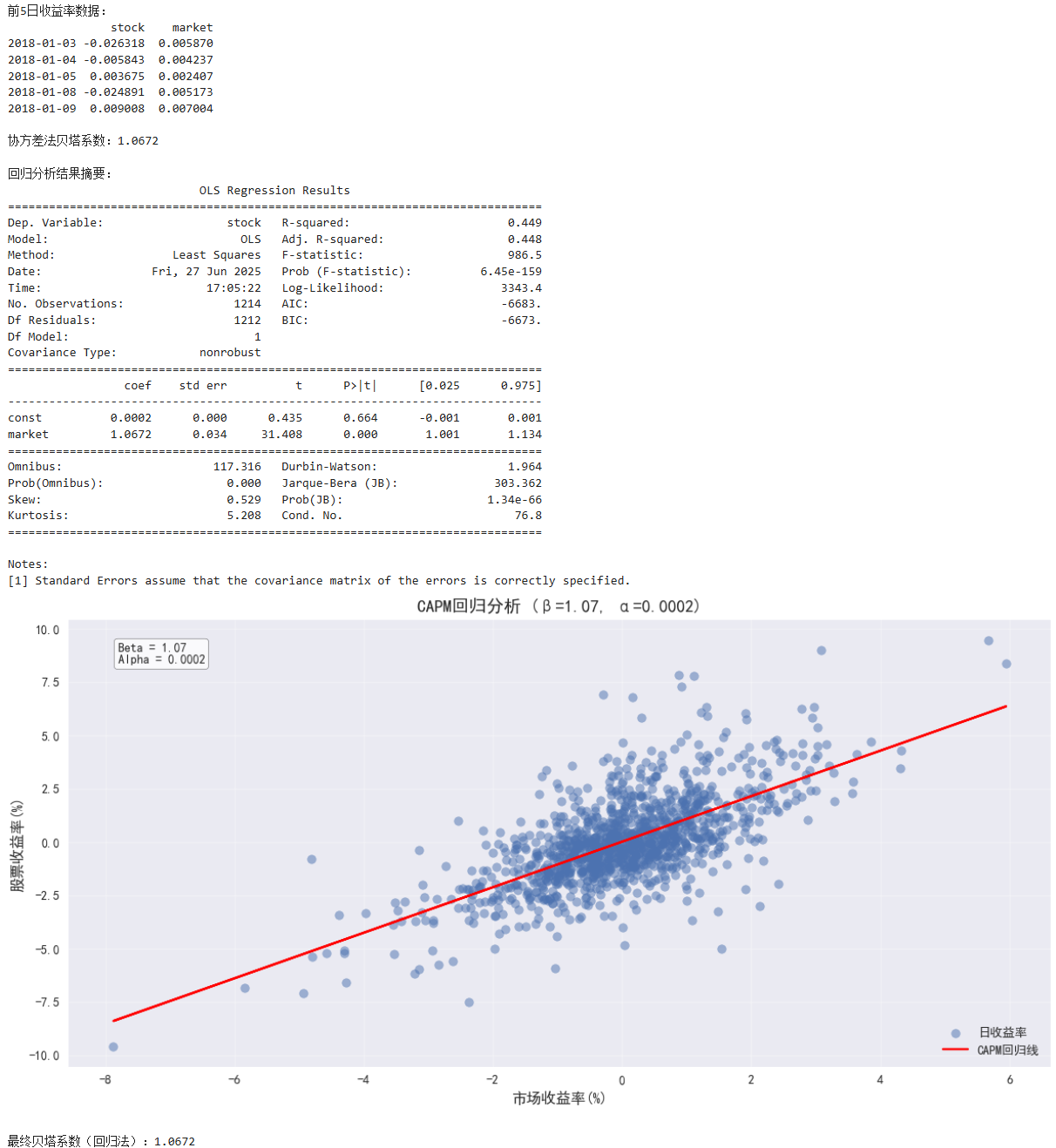

| import pandas as pd

import statsmodels.api as sm

import matplotlib.pyplot as plt

# 1. 数据预处理

# 合并股票和沪深300数据

merged_df = pd.concat([df['收盘'], hs300['close']], axis=1)

merged_df.columns = ['stock', 'market']

# 计算日收益率(使用对数收益率更符合金融特性)

returns = merged_df.pct_change().dropna()

# returns = np.log(merged_df / merged_df.shift(1)).dropna() # 对数收益率

print("前5日收益率数据:")

print(returns.head())

# 2. 协方差法计算贝塔

cov_matrix = returns.cov()

cov_stock_market = cov_matrix.loc['stock', 'market'] # 股票与市场的协方差

market_variance = returns['market'].var() # 市场方差

beta_cov = cov_stock_market / market_variance

print(f"\n协方差法贝塔系数:{beta_cov:.4f}")

# 3. 回归法计算贝塔(CAPM标准方法)

# 准备回归数据

X = returns['market'] # 自变量:市场收益率

y = returns['stock'] # 因变量:股票收益率

X = sm.add_constant(X) # 添加截距项

# 拟合线性回归模型

model = sm.OLS(y, X).fit()

beta_regression = model.params['market']

alpha = model.params['const']

# 输出回归结果

print("\n回归分析结果摘要:")

print(model.summary())

# 4. 可视化分析

plt.figure(figsize=(12, 6))

# 绘制收益率散点图与回归线

plt.scatter(returns['market']*100, returns['stock']*100, alpha=0.5, label='日收益率')

plt.plot(returns['market']*100, (alpha + beta_regression*returns['market'])*100,

color='red', label='CAPM回归线')

plt.xlabel('市场收益率(%)', fontsize=12)

plt.ylabel('股票收益率(%)', fontsize=12)

plt.title(f'CAPM回归分析 (β={beta_regression:.2f}, α={alpha:.4f})', fontsize=14)

plt.legend()

plt.grid(alpha=0.3)

# 添加Beta值标注

plt.text(0.05, 0.95,

f'Beta = {beta_regression:.2f}\nAlpha = {alpha:.4f}',

transform=plt.gca().transAxes,

verticalalignment='top',

bbox=dict(boxstyle='round', facecolor='white', alpha=0.8))

plt.tight_layout()

plt.show()

# 5. 输出最终贝塔系数

print(f"\n最终贝塔系数(回归法):{beta_regression:.4f}")

|