1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142

143

| import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

from matplotlib.ticker import FuncFormatter

# 运行模拟

simulated_paths = geometric_brownian_motion(S_0, mu, sigma, N_SIM, T, N)

# 创建与测试集对应的时间索引

date_index = pd.date_range(start=train.index[-1], periods=N+1, freq='D')[:N+1]

# ======================

# 可视化部分

# ======================

# 1. 模拟路径与真实价格对比

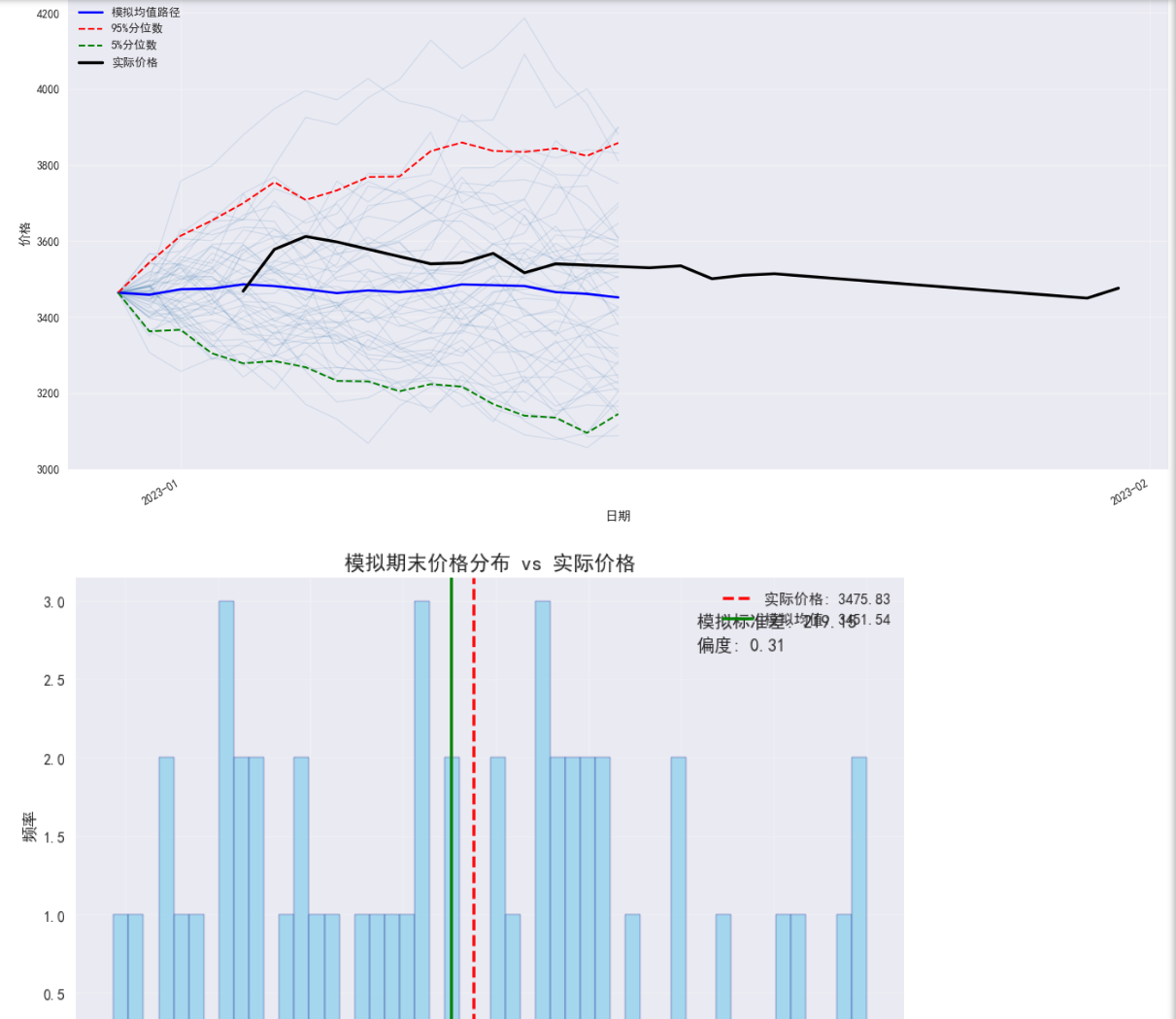

plt.figure(figsize=(14, 7))

plt.title(f"股票价格蒙特卡洛模拟 (N={N_SIM}次)\nμ={mu:.4f}, σ={sigma:.4f}", fontsize=14)

# 绘制所有模拟路径(半透明处理)

for i in range(N_SIM):

plt.plot(date_index, simulated_paths[i], lw=1, alpha=0.15, color='steelblue')

# 计算并绘制关键统计量

mean_path = np.mean(simulated_paths, axis=0)

upper_95 = np.percentile(simulated_paths, 95, axis=0)

lower_5 = np.percentile(simulated_paths, 5, axis=0)

plt.plot(date_index, mean_path, 'b-', lw=2, label='模拟均值路径')

plt.plot(date_index, upper_95, 'r--', lw=1.5, label='95%分位数')

plt.plot(date_index, lower_5, 'g--', lw=1.5, label='5%分位数')

# 添加实际价格曲线(测试期)

test_period = df.loc[test.index, '收盘']

plt.plot(test_period.index, test_period.values, 'k-', lw=2.5, label='实际价格')

# 美化坐标轴

plt.gca().xaxis.set_major_locator(mdates.MonthLocator())

plt.gca().xaxis.set_major_formatter(mdates.DateFormatter('%Y-%m'))

plt.gcf().autofmt_xdate() # 自动旋转日期标签

# 添加图例和网格

plt.legend(loc='upper left')

plt.grid(True, alpha=0.3)

plt.xlabel('日期')

plt.ylabel('价格')

plt.tight_layout()

plt.savefig('GBM_模拟路径对比.png', dpi=300)

plt.show()

# 2. 模拟路径与真实价格差异分析(最后一天)

final_prices = simulated_paths[:, -1]

actual_final_price = test_period.iloc[-1]

plt.figure(figsize=(10, 6))

plt.hist(final_prices, bins=50, alpha=0.7, color='skyblue', edgecolor='navy')

plt.axvline(x=actual_final_price, color='red', linestyle='--', lw=2,

label=f'实际价格: {actual_final_price:.2f}')

plt.axvline(x=np.mean(final_prices), color='green', linestyle='-', lw=2,

label=f'模拟均值: {np.mean(final_prices):.2f}')

# 添加统计指标

plt.text(0.75, 0.9, f'模拟标准差: {np.std(final_prices):.2f}',

transform=plt.gca().transAxes, fontsize=12)

plt.text(0.75, 0.85, f'偏度: {pd.Series(final_prices).skew():.2f}',

transform=plt.gca().transAxes, fontsize=12)

plt.title('模拟期末价格分布 vs 实际价格', fontsize=14)

plt.xlabel('期末价格')

plt.ylabel('频率')

plt.legend()

plt.grid(alpha=0.2)

plt.savefig('GBM_期末价格分布.png', dpi=300)

plt.show()

# 3. 动态预测区间(随时间变化的置信区间)

plt.figure(figsize=(14, 7))

plt.fill_between(date_index,

np.percentile(simulated_paths, 5, axis=0),

np.percentile(simulated_paths, 95, axis=0),

color='lightblue', alpha=0.5, label='90%置信区间')

plt.plot(date_index, mean_path, 'b-', lw=2, label='模拟均值')

plt.plot(test_period.index, test_period.values, 'k-', lw=2.5, label='实际价格')

# 标记关键事件点

max_dev_idx = np.argmax(np.abs(test_period.values - mean_path[1:]))

event_date = test_period.index[max_dev_idx]

plt.axvline(x=event_date, color='purple', linestyle=':', alpha=0.8)

plt.text(event_date, plt.ylim()[0]*0.95, f'最大偏离点\n{event_date.strftime("%Y-%m-%d")}',

ha='center', fontsize=9)

plt.title('GBM模拟的90%置信区间与实际价格对比', fontsize=14)

plt.xlabel('日期')

plt.ylabel('价格')

plt.legend(loc='upper left')

plt.gca().xaxis.set_major_locator(mdates.MonthLocator(interval=2))

plt.gca().xaxis.set_major_formatter(mdates.DateFormatter('%Y-%m'))

plt.gcf().autofmt_xdate()

plt.grid(alpha=0.3)

plt.tight_layout()

plt.savefig('GBM_动态置信区间.png', dpi=300)

plt.show()

# 4. 计算预测误差指标

simulated_mean = mean_path[1:]

actual_prices = test_period.values

mae = np.mean(np.abs(simulated_mean - actual_prices))

rmse = np.sqrt(np.mean((simulated_mean - actual_prices)**2))

print("\n模型性能评估:")

print(f"平均绝对误差(MAE): {mae:.4f}")

print(f"均方根误差(RMSE): {rmse:.4f}")

print(f"年化波动率预测: {sigma:.4f} (实际: {test.std()*np.sqrt(252):.4f})")

# 5. 关键日期对比表

compare_dates = [test_period.index[0], test_period.index[len(test)//2], test_period.index[-1]]

compare_data = []

valid_dates = [d for d in compare_dates if d in date_index]

# valid_dates

for date in valid_dates:

idx = np.where(date_index == date)[0][0]

actual = df.loc[date, '收盘']

sim_mean = mean_path[idx]

sim_median = np.median(simulated_paths[:, idx])

compare_data.append([

date.strftime('%Y-%m-%d'),

actual,

sim_mean,

sim_median,

actual - sim_mean

])

# 创建对比表格

compare_df = pd.DataFrame(compare_data,

columns=['日期', '实际价格', '模拟均值', '模拟中位数', '偏差'])

print("\n关键日期价格对比:")

print(compare_df.to_string(index=False))

|