1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

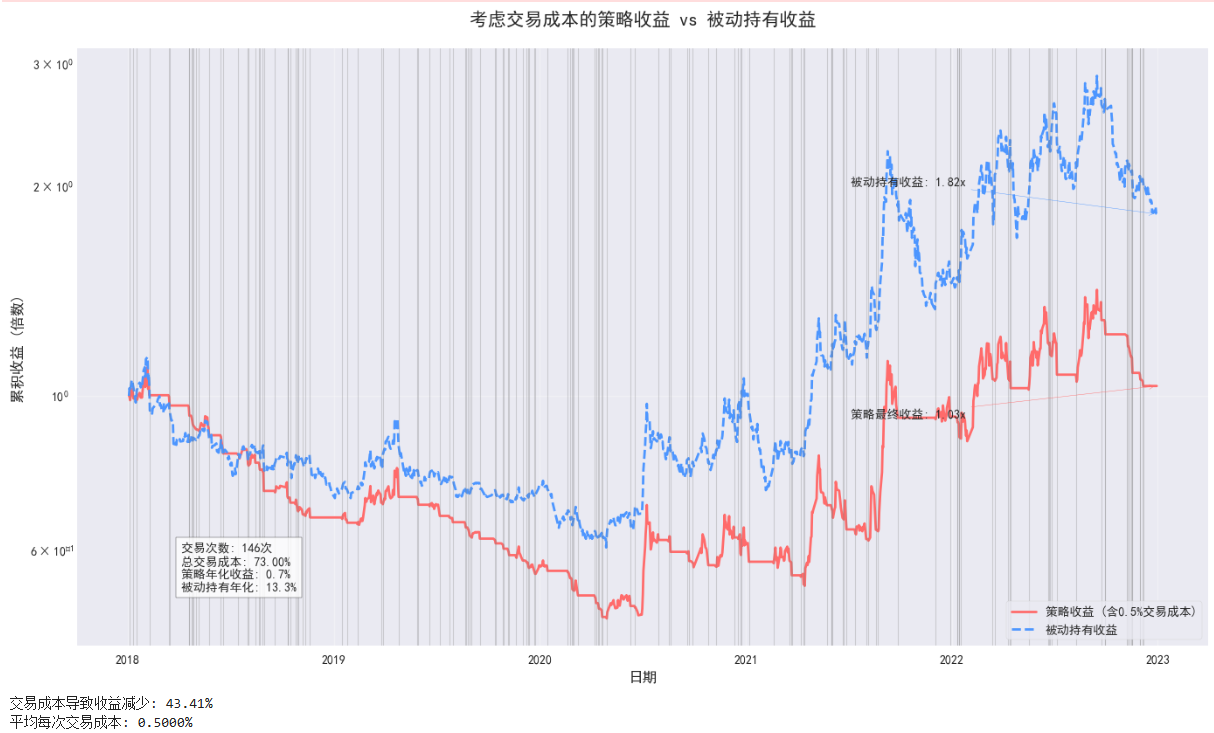

| import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

# 计算20日均线

price['short_mavg'] = price['收盘'].rolling(window=20, min_periods=1).mean()

# 生成交易信号 (收盘价上穿20日均线买入,否则卖出)

price['signal'] = 0.0

price['signal'] = np.where(price['收盘'] > price['short_mavg'], 1.0, 0.0)

# 计算每日收益

price['daily_returns'] = price['收盘'].pct_change()

# ===== 添加交易成本计算 =====

# 计算仓位变化 (信号变化时产生交易)

price['position_change'] = price['signal'].diff().abs()

# 计算交易成本 (0.5%的单向费率)

price['trading_cost'] = price['position_change'] * 0.005

# 计算策略收益 (扣除交易成本)

price['strategy_returns'] = price['daily_returns'] * price['signal'].shift(1) - price['trading_cost']

# 计算被动持有收益 (无交易成本)

price['benchmark_returns'] = price['daily_returns']

# ===== 计算累积收益 =====

# 策略累积收益 (考虑交易成本)

price['cumulative_strategy_returns'] = (1 + price['strategy_returns']).cumprod()

# 被动持有累积收益

price['cumulative_benchmark_returns'] = (1 + price['benchmark_returns']).cumprod()

# ===== 可视化对比 =====

plt.figure(figsize=(14, 8), dpi=100)

plt.grid(True, alpha=0.3)

# 绘制累积收益曲线

plt.plot(price.index, price['cumulative_strategy_returns'],

label='策略收益 (含0.5%交易成本)', lw=2, color='#FF6B6B')

plt.plot(price.index, price['cumulative_benchmark_returns'],

label='被动持有收益', ls='--', lw=2, color='#4D96FF')

# 标记交易点

trade_dates = price[price['position_change'] > 0].index

for date in trade_dates:

plt.axvline(x=date, color='gray', alpha=0.3, lw=0.8)

# 添加最终收益标注

final_strategy = price['cumulative_strategy_returns'].iloc[-1]

final_benchmark = price['cumulative_benchmark_returns'].iloc[-1]

plt.annotate(f'策略最终收益: {final_strategy:.2f}x',

xy=(price.index[-1], final_strategy),

xytext=(price.index[-int(len(price)*0.3)], final_strategy*0.9),

arrowprops=dict(arrowstyle='->', color='#FF6B6B'))

plt.annotate(f'被动持有收益: {final_benchmark:.2f}x',

xy=(price.index[-1], final_benchmark),

xytext=(price.index[-int(len(price)*0.3)], final_benchmark*1.1),

arrowprops=dict(arrowstyle='->', color='#4D96FF'))

# 添加统计信息

trade_count = len(trade_dates)

total_cost = price['trading_cost'].sum() * 100

plt.figtext(0.15, 0.15,

f"交易次数: {trade_count}次\n总交易成本: {total_cost:.2f}%\n"

f"策略年化收益: {final_strategy**(252/len(price))-1:.1%}\n"

f"被动持有年化: {final_benchmark**(252/len(price))-1:.1%}",

bbox=dict(facecolor='white', alpha=0.8))

# 设置图表元素

plt.title('考虑交易成本的策略收益 vs 被动持有收益', fontsize=15, pad=20)

plt.xlabel('日期', fontsize=12)

plt.ylabel('累积收益 (倍数)', fontsize=12)

plt.legend(loc='best', frameon=True)

plt.yscale('log') # 对数刻度更好展示长期收益

plt.tight_layout()

plt.savefig('考虑交易成本的收益对比.jpg', dpi=300, bbox_inches='tight')

plt.show()

# ===== 额外分析:交易成本影响 =====

cost_impact = (final_benchmark - final_strategy) / final_benchmark * 100

print(f"交易成本导致收益减少: {cost_impact:.2f}%")

print(f"平均每次交易成本: {total_cost/trade_count:.4f}%")

|