1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

| import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

import matplotlib.ticker as mtick

# 计算移动平均线

price['short_mavg'] = price['收盘'].rolling(window=20, min_periods=1).mean()

price['long_mavg'] = price['收盘'].rolling(window=100, min_periods=1).mean()

# 生成交易信号

price['signal'] = 0.0

price['signal'] = np.where(price['short_mavg'] > price['long_mavg'], 1.0, 0.0)

# 计算每日收益率

price['daily_return'] = price['收盘'].pct_change()

# 计算策略收益

price['strategy_position'] = price['signal'].shift(1) # 使用前一天的信号避免未来函数

price['strategy_return'] = price['strategy_position'] * price['daily_return']

price['strategy_cumulative'] = (1 + price['strategy_return']).cumprod()

# 计算被动持有收益

price['buy_hold_return'] = price['daily_return']

price['buy_hold_cumulative'] = (1 + price['buy_hold_return']).cumprod()

# 计算累计收益

initial_value = 10000 # 假设初始投资10000元

price['strategy_value'] = initial_value * price['strategy_cumulative']

price['buy_hold_value'] = initial_value * price['buy_hold_cumulative']

# 设置绘图风格

plt.style.use('seaborn-v0_8')

#指定字体,防止中文出现乱码,windows系统指定为‘SimHei’

plt.rcParams['font.sans-serif'] = ['SimHei']

#这行代码让中文的负号“-”可以正常显示

plt.rcParams["axes.unicode_minus"]=False

# 创建图表

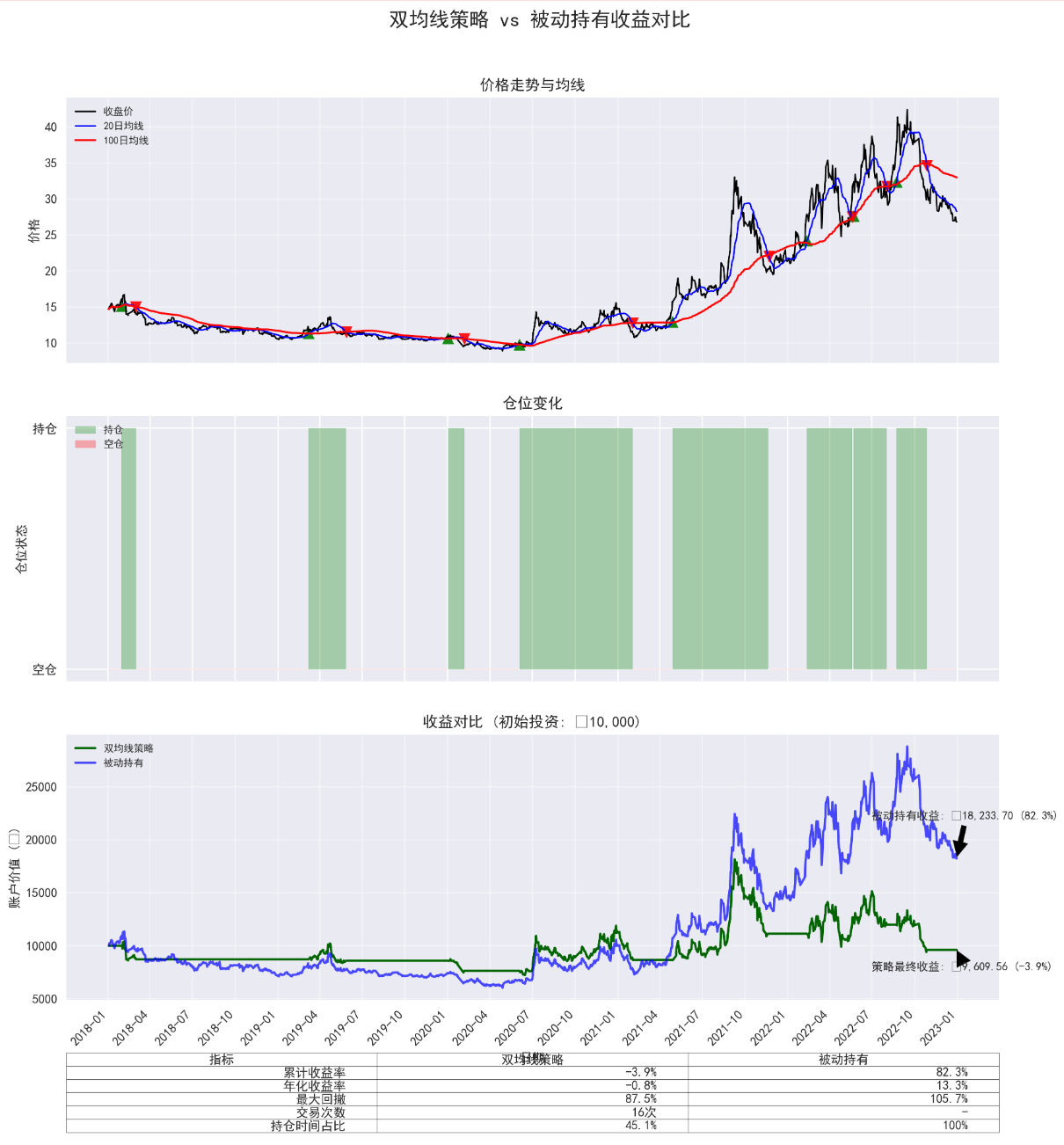

fig, (ax1, ax2, ax3) = plt.subplots(3, 1, figsize=(12, 12), dpi=300, sharex=True)

fig.suptitle('双均线策略 vs 被动持有收益对比', fontsize=16, fontweight='bold')

# 绘制价格和均线

ax1.plot(price.index, price['收盘'], label='收盘价', lw=1.2, color='black')

ax1.plot(price.index, price['short_mavg'], label='20日均线', lw=1.2, color='blue')

ax1.plot(price.index, price['long_mavg'], label='100日均线', lw=1.5, color='red')

ax1.set_title('价格走势与均线', fontsize=12)

ax1.set_ylabel('价格', fontsize=10)

ax1.legend(loc='upper left', fontsize=8)

ax1.grid(True, alpha=0.4)

# 标记金叉死叉点

gold_cross = price[(price['short_mavg'] > price['long_mavg']) &

(price['short_mavg'].shift(1) <= price['long_mavg'].shift(1))]

death_cross = price[(price['short_mavg'] < price['long_mavg']) &

(price['short_mavg'].shift(1) >= price['long_mavg'].shift(1))]

ax1.scatter(gold_cross.index, gold_cross['short_mavg'],

marker='^', s=80, color='green', alpha=0.9, label='金叉(买入)')

ax1.scatter(death_cross.index, death_cross['short_mavg'],

marker='v', s=80, color='red', alpha=0.9, label='死叉(卖出)')

# 绘制仓位变化

ax2.fill_between(price.index, price['signal'],

color='green', alpha=0.3,

where=(price['signal'] == 1.0), label='持仓')

ax2.fill_between(price.index, price['signal'],

color='red', alpha=0.3,

where=(price['signal'] == 0.0), label='空仓')

ax2.set_title('仓位变化', fontsize=12)

ax2.set_ylabel('仓位状态', fontsize=10)

ax2.set_yticks([0, 1])

ax2.set_yticklabels(['空仓', '持仓'])

ax2.legend(loc='upper left', fontsize=8)

# 绘制收益对比

ax3.plot(price.index, price['strategy_value'],

label='双均线策略', lw=1.8, color='darkgreen')

ax3.plot(price.index, price['buy_hold_value'],

label='被动持有', lw=1.8, color='blue', alpha=0.7)

ax3.set_title('收益对比 (初始投资: ¥10,000)', fontsize=12)

ax3.set_ylabel('账户价值 (¥)', fontsize=10)

ax3.set_xlabel('日期', fontsize=10)

ax3.legend(loc='upper left', fontsize=8)

ax3.grid(True, alpha=0.4)

# 添加最终收益标注

final_strategy = price['strategy_value'].iloc[-1]

final_buy_hold = price['buy_hold_value'].iloc[-1]

strategy_return_pct = (final_strategy - initial_value) / initial_value * 100

buy_hold_return_pct = (final_buy_hold - initial_value) / initial_value * 100

ax3.annotate(f'策略最终收益: ¥{final_strategy:,.2f} ({strategy_return_pct:.1f}%)',

xy=(price.index[-1], final_strategy),

xytext=(price.index[-1] - pd.DateOffset(months=6), final_strategy * 0.8),

arrowprops=dict(facecolor='black', shrink=0.05),

fontsize=9)

ax3.annotate(f'被动持有收益: ¥{final_buy_hold:,.2f} ({buy_hold_return_pct:.1f}%)',

xy=(price.index[-1], final_buy_hold),

xytext=(price.index[-1] - pd.DateOffset(months=6), final_buy_hold * 1.2),

arrowprops=dict(facecolor='black', shrink=0.05),

fontsize=9)

# 设置x轴日期格式

ax3.xaxis.set_major_locator(mdates.MonthLocator(interval=3))

ax3.xaxis.set_major_formatter(mdates.DateFormatter('%Y-%m'))

plt.xticks(rotation=45, ha='right')

# 调整布局

plt.tight_layout(rect=[0, 0, 1, 0.96]) # 为总标题留空间

plt.subplots_adjust(hspace=0.2) # 调整子图间距

# 添加统计信息表格

stats_data = [

["累计收益率", f"{strategy_return_pct:.1f}%", f"{buy_hold_return_pct:.1f}%"],

["年化收益率",

f"{(price['strategy_cumulative'].iloc[-1] ** (252/len(price)) - 1) * 100:.1f}%",

f"{(price['buy_hold_cumulative'].iloc[-1] ** (252/len(price)) - 1) * 100:.1f}%"],

["最大回撤",

f"{((price['strategy_value'].cummax() - price['strategy_value']).max() / initial_value * 100):.1f}%",

f"{((price['buy_hold_value'].cummax() - price['buy_hold_value']).max() / initial_value * 100):.1f}%"],

["交易次数", f"{len(gold_cross) + len(death_cross)}次", "-"],

["持仓时间占比", f"{price['signal'].mean() * 100:.1f}%", "100%"]

]

table = plt.table(cellText=stats_data,

colLabels=['指标', '双均线策略', '被动持有'],

loc='bottom',

bbox=[0, -0.5, 1, 0.3])

table.auto_set_font_size(False)

table.set_fontsize(10)

table.scale(1, 1.5)

# 保存和显示

plt.savefig('收益对比分析.jpg', dpi=300, bbox_inches='tight')

plt.show()

|