AI实现CCC-GARCH模型

编辑

2

2025-06-29

提示词

# Python代码

# 读取下载的Excel文件并处理

df = pd.read_excel('../数据/棉花十年行情数据.xlsx')#换成你保存文件的路径

df = df[['日期', '收盘价']]

df.set_index('日期', inplace=True)

#检查数据

df.tail()

# Python代码

# 读取棕榈油期货行情数据Excel文件

df2 = pd.read_excel('../数据/棕榈油十年行情数据.xlsx', index_col='日期')

df2 = df2['收盘价']

# df是棉花期货的收盘价

# 将两个期货的收盘价合并进一个dataframe

df = df.join(df2, lsuffix='棉花',rsuffix='棕榈油')

# 检查结果

df.tail()

# Python代码

# 计算两种期货的价格变动

returns = df.pct_change().dropna()*100

# 重命名列名

returns.columns = ['棉花期货涨跌', '棕榈油期货涨跌']

# 数据可视化

returns.plot(subplots=True, figsize=(15,10))

plt.title('两种期货的价格波动', fontsize=20)

plt.savefig('图9-5.jpg',dpi=300)

plt.show()

使用上面的returns DataFrame,分别用两种期货的行情数据拟合GARCH模型,并将模型的系数、条件波动性、标准化残差和模型本身保存在不同的列表中,请给出示例代码。

答案

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from arch import arch_model

# 1. 数据准备(已加载returns DataFrame)

# 假设returns DataFrame包含'棉花期货涨跌'和'棕榈油期货涨跌'两列收益率数据

print(returns.head())

# 2. 初始化存储结果的列表

model_params = [] # 存储模型系数

cond_volatility = [] # 存储条件波动性

std_residuals = [] # 存储标准化残差

garch_models = [] # 存储模型对象本身

model_summaries = [] # 存储模型摘要

forecast_results = [] # 存储预测结果

# 3. 对每个期货品种拟合GARCH模型

commodities = ['棉花期货涨跌', '棕榈油期货涨跌']

for commodity in commodities:

print(f"\n{'='*50}")

print(f"拟合{commodity}的GARCH模型...")

print('='*50)

# 3.1 拟合GARCH(1,1)模型[1,5,10](@ref)

model = arch_model(

returns[commodity].dropna(),

mean='Constant', # 常数均值模型

vol='Garch', # GARCH波动率模型

p=1, # GARCH阶数

q=1, # ARCH阶数

dist='StudentsT' # 使用学生t分布考虑厚尾特征[4](@ref)

)

# 3.2 模型拟合[2,6](@ref)

result = model.fit(disp='off', show_warning=False)

# 3.3 保存模型对象

garch_models.append(result)

# 3.4 保存模型系数[1,10](@ref)

params = result.params

model_params.append(params)

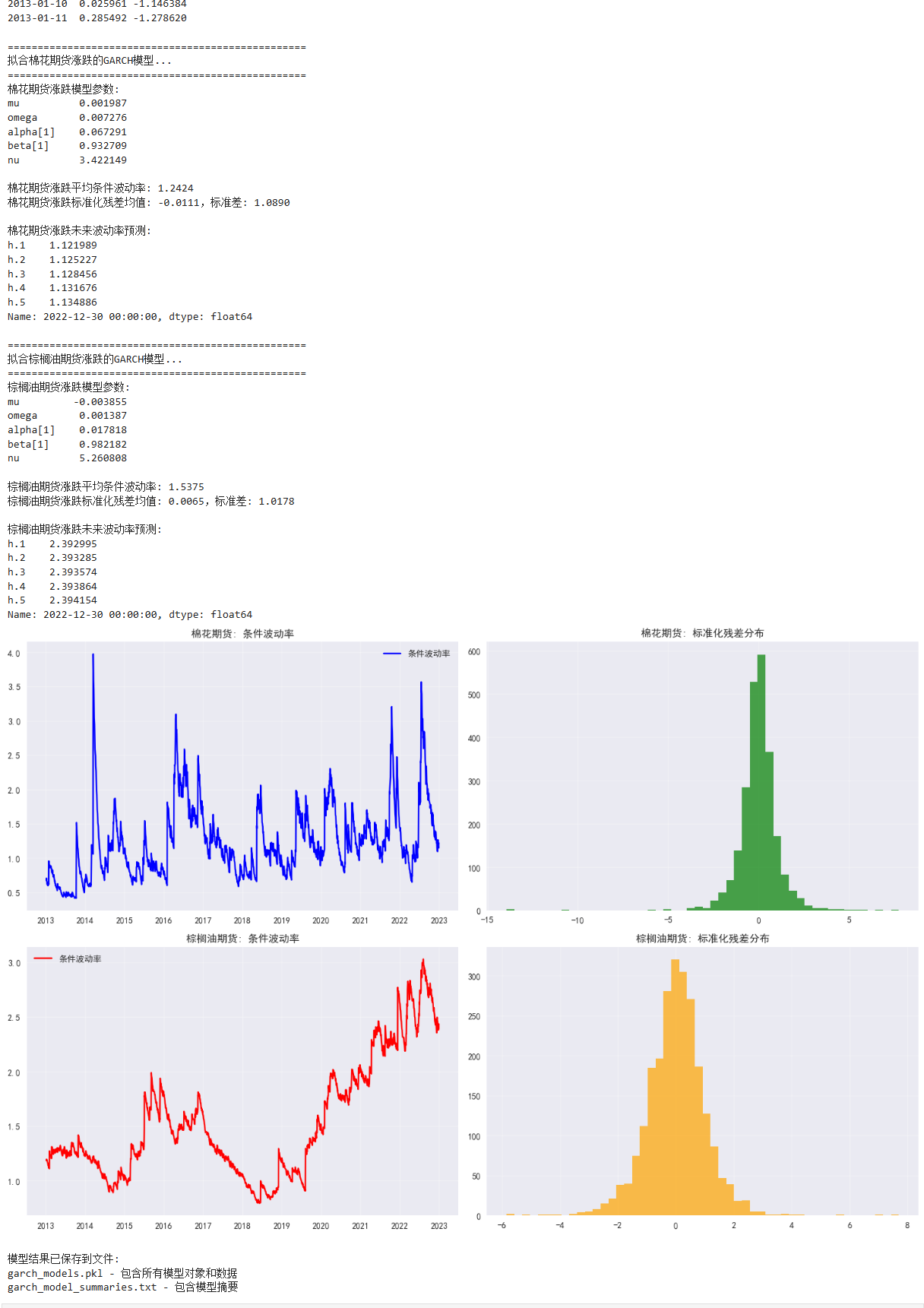

print(f"{commodity}模型参数:")

print(params.to_string())

# 3.5 保存条件波动性[1,7](@ref)

vol_series = result.conditional_volatility

cond_volatility.append(vol_series)

print(f"\n{commodity}平均条件波动率: {vol_series.mean():.4f}")

# 3.6 计算并保存标准化残差[7,8](@ref)

resid = result.resid

std_resid = resid / vol_series

std_residuals.append(std_resid)

print(f"{commodity}标准化残差均值: {std_resid.mean():.4f},标准差: {std_resid.std():.4f}")

# 3.7 保存模型摘要

model_summaries.append(result.summary())

# 3.8 波动率预测(未来5天)[1](@ref)

forecast = result.forecast(horizon=5)

forecast_results.append(forecast)

print(f"\n{commodity}未来波动率预测:")

print(np.sqrt(forecast.variance.iloc[-1]))

# 4. 结果可视化

plt.figure(figsize=(15, 10))

# 4.1 棉花期货结果

plt.subplot(2, 2, 1)

plt.plot(cond_volatility[0], label='条件波动率', color='blue')

plt.title('棉花期货: 条件波动率', fontsize=12)

plt.grid(alpha=0.3)

plt.legend()

plt.subplot(2, 2, 2)

plt.hist(std_residuals[0], bins=50, alpha=0.7, color='green')

plt.title('棉花期货: 标准化残差分布', fontsize=12)

plt.grid(alpha=0.3)

# 4.2 棕榈油期货结果

plt.subplot(2, 2, 3)

plt.plot(cond_volatility[1], label='条件波动率', color='red')

plt.title('棕榈油期货: 条件波动率', fontsize=12)

plt.grid(alpha=0.3)

plt.legend()

plt.subplot(2, 2, 4)

plt.hist(std_residuals[1], bins=50, alpha=0.7, color='orange')

plt.title('棕榈油期货: 标准化残差分布', fontsize=12)

plt.grid(alpha=0.3)

plt.tight_layout()

plt.savefig('garch_model_results.png', dpi=300)

plt.show()

# 5. 模型保存(可选)[3](@ref)

import joblib

# 5.1 保存模型对象

model_data = {

'commodities': commodities,

'params': model_params,

'cond_volatility': cond_volatility,

'std_residuals': std_residuals,

'models': garch_models

}

joblib.dump(model_data, 'garch_models.pkl')

# 5.2 保存模型摘要文本

with open('garch_model_summaries.txt', 'w') as f:

for i, summary in enumerate(model_summaries):

f.write(f"{'='*50}\n")

f.write(f"{commodities[i]} GARCH模型摘要\n")

f.write(f"{'='*50}\n\n")

f.write(str(summary))

f.write("\n\n\n")

print("\n模型结果已保存到文件:")

print("garch_models.pkl - 包含所有模型对象和数据")

print("garch_model_summaries.txt - 包含模型摘要")

结果:

计算恒定条件相关性矩阵

提示词

简化代码加描述

# Python代码

# 'returns' 包含 '棉花期货涨跌' 和 '棕榈油期货涨跌' 列

# 初始化空列表用于保存结果

model_coeffs = []

conditional_volatility = []

standard_resid = []

garch_models = []

# 提取列名,即两种期货的名称

columns = returns.columns

# 遍历每个期货,拟合 GARCH 模型并保存结果

for column in columns:

# 创建 GARCH 模型

model = arch_model(returns[column], vol='Garch', p=1, q=1)

# 拟合模型

result = model.fit(update_freq=0, disp="off")

# 将结果保存到相应的列表中

model_coeffs.append(result.params)

conditional_volatility.append(result.conditional_volatility)

standard_resid.append(result.std_resid)

garch_models.append(result)

# 将模型系数转化为dataframe

coeffs_df = pd.DataFrame(model_coeffs, index=columns)

# 检查结果

coeffs_df

现在要基于上面代码中的standard_resid计算恒定条件相关性矩阵,请给出示例代码。

答案

import numpy as np

import pandas as pd

# 1. 将标准化残差组合成DataFrame

# 假设standard_resid是包含两个期货品种标准化残差的列表

std_resid_df = pd.DataFrame({

'棉花标准化残差': standard_resid[0],

'棕榈油标准化残差': standard_resid[1]

}, index=returns.index) # 使用原始收益率数据的索引

# 2. 计算恒定条件相关系数

# CCC矩阵的核心是计算标准化残差的样本相关系数

ccc_matrix = std_resid_df.corr()

# 3. 输出CCC矩阵

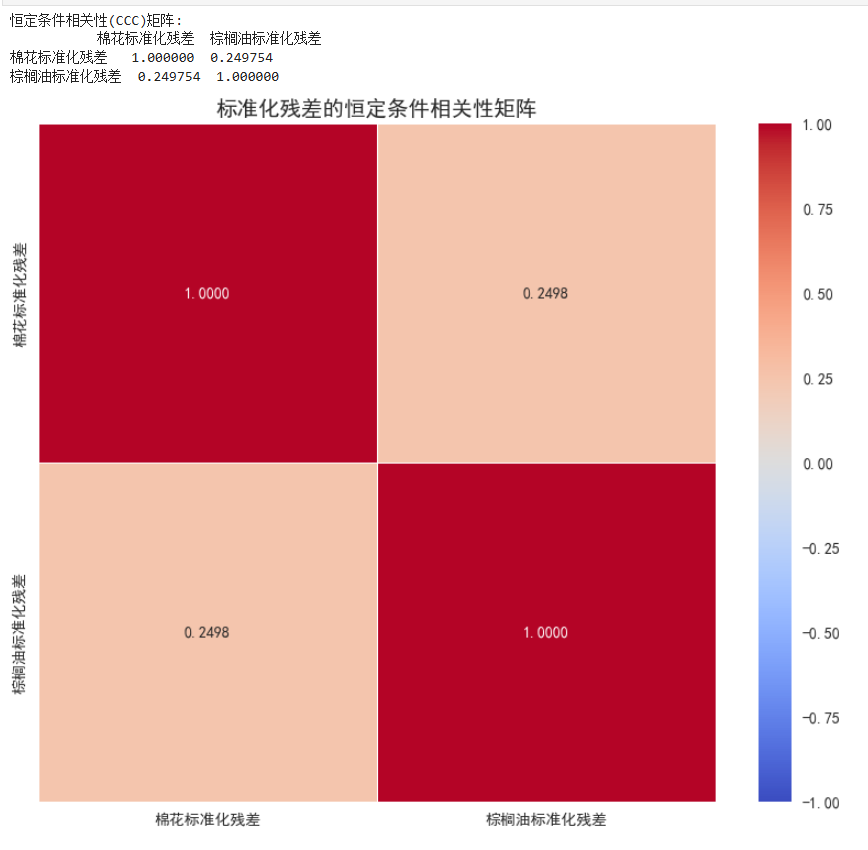

print("恒定条件相关性(CCC)矩阵:")

print(ccc_matrix)

# 4. 高级可视化(使用热力图展示)

import seaborn as sns

import matplotlib.pyplot as plt

plt.figure(figsize=(10, 8))

sns.heatmap(

ccc_matrix,

annot=True, # 显示数值

cmap='coolwarm', # 冷暖色系区分正负相关

vmin=-1, vmax=1, # 相关系数范围

square=True, # 单元格为正方形

fmt=".4f", # 显示4位小数

linewidths=0.5 # 单元格边界线宽

)

plt.title('标准化残差的恒定条件相关性矩阵', fontsize=14)

plt.savefig('ccc_correlation_matrix.png', dpi=300, bbox_inches='tight')

plt.show()

结果:

- 0

- 0

-

赞助

支付宝

支付宝

微信

微信

-

分享